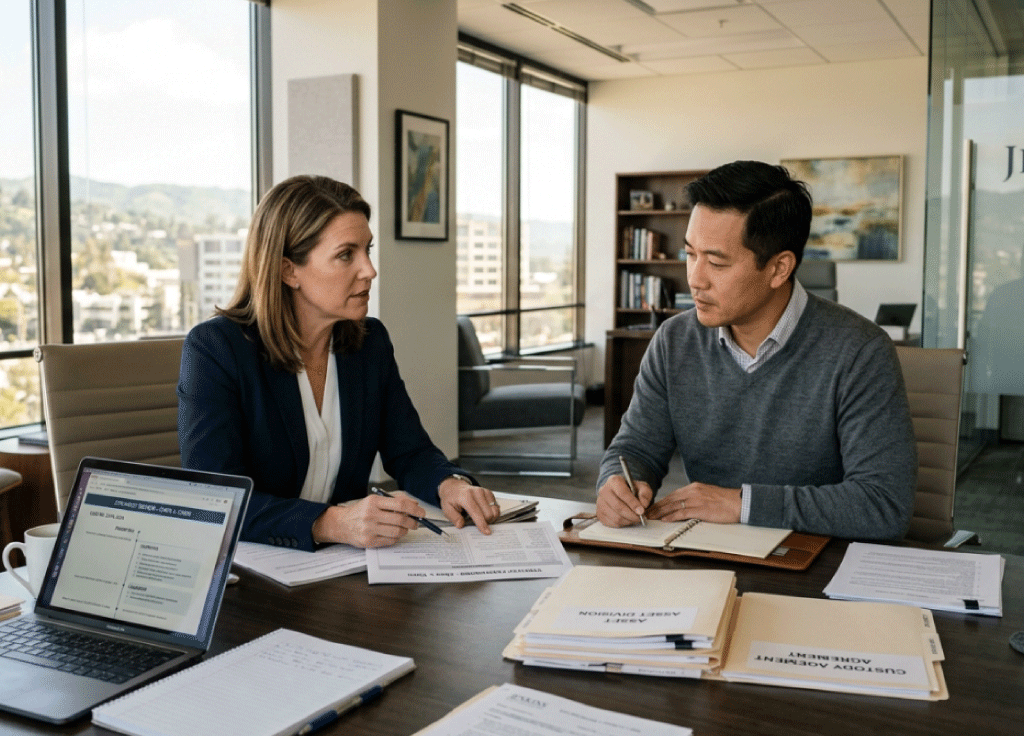

Splitting Retirement Accounts with Qualified Domestic Relations Orders

In a Community Property state like California, your ex-spouse or domestic partner is entitled to 50% of the value that you have accumulated in your employee sponsored retirement accounts during your marriage. These retirement accounts can be a 401K plan, IRA or pension plan.

Retirement accounts are governed by many laws, including federal tax laws. A Qualified Domestic Relations Order (QDRO) is a type of court order that complies with federal law in determining how your retirement accounts will be divided when you divorce. With a QDRO in place, after your retirement accounts are divided, your former spouse will be responsible for any of the taxes due on the portion of the accounts that he or she has received. A QDRO also allows your ex-spouse to roll over the divided portion of your retirement accounts into an IRA without penalty or taxes. The QDRO must be worded appropriately, so that the retirement plan administrator can transfer the funds tax free.

Without a QDRO in place, the holder of the retirement accounts (you) will be responsible for the taxes due on the amount that is transferred to your ex-spouse.

Along with using a QDRO to divide marital assets during divorce, Qualified Domestic Relations Orders may also be used to pay child support or spousal support from retirement accounts.

Following are some things to be aware of with a QDRO:

Be sure to use the right account transfer language – The IRA transfer should be “trustee to trustee,” rather than made directly to your ex-spouse, in other words Charles Schwab as Trustee to Charles Schwab as Trustee. By using trustee to trustee, the funds transfer as a non-taxable transaction, and there is no 10% penalty, if your ex-spouse is younger than 59 1/2. Your ex-spouse will pay ordinary income taxes, whenever he or she uses the funds.

If you are transferring an entire IRA to your ex-spouse, a QDRO is not necessary. Instead, the custodian may require only your divorce decree or marital settlement agreement to transfer the account. This will both save on legal fees and allow the assets to transfer quickly.

Pension retirement account division rules differ by company – The wording of the QDRO for your pension should be driven by your company’s rules. Some organizations will immediately transfer the divided pension to your ex-spouse. Other organizations will pay your ex when the pension is eligible for distribution. You should check with your pension plan administrator as to how your pension will be distributed.

If you are the recipient of the retirement account portion and need the cash – If you are younger than 59 1/2 and need to use the funds right now for things like buying your former spouse out of your house, instead of rolling the funds into an IRA, you can have the QDRO written so that you will get a taxable, penalty free distribution. In other words, you will need to pay ordinary income taxes, but no early withdrawal penalty. Otherwise, taking an early withdrawal from a retirement account before you are 59 1/2 will result in a 10% tax penalty, in addition to paying ordinary income taxes for the amount you withdraw.

Contact me for assistance

If you are getting a divorce, need to determine the best way to divide your retirement assets, and live in the San Francisco Bay Area, please contact my office for a consultation. As an divorce attorney, I would be happy to provide expert legal advice. Ideally, your QDRO would be ready to be entered with the court at the same time as your divorce judgment.

Warren Major LLP is a Marin County CA family law firm specializing in divorce, child custody and support, marital contracts and other family law issues.

Disclaimer:Warren Major LLP publishes articles about family law cases on its website for informational purposes only. The information contained herein may not reflect the current law in your jurisdiction. No information contained in this post should be construed as legal advice from Warren Major LLP or the individual author. This general information is not a substitute for legal advice on any subject matter. For advice pertaining to your specific case, please contact our office to schedule a consultation. No reader of this article should act or refrain from acting on the basis of any information included in, or accessible through, this article without seeking the appropriate legal or other professional advice on the particular facts and circumstances at issue from a lawyer licensed in the recipient’s state, country or other appropriate licensing jurisdiction. Using this information or sending electronic mail to Warren Major LLP or its attorneys does not create an attorney-client relationship. Any statements pertaining to past results do not guarantee future results.